Why is it that recent acquisitions in the crypto space no longer include the token?

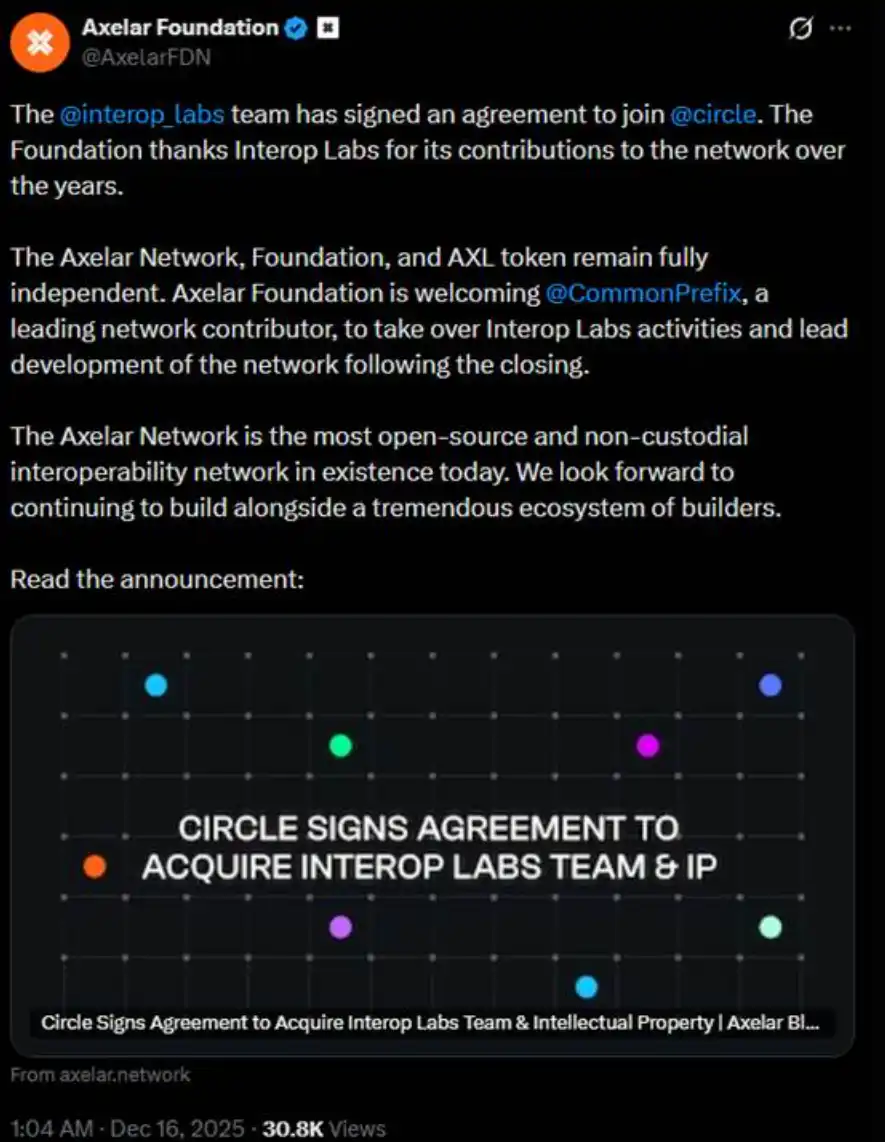

The day before yesterday, the Interop Labs team (the original developers of the Axelar Network) announced their acquisition by Circle to accelerate the development of their multi-chain infrastructure Arc and CCTP.

Normally, getting acquired is a good thing. However, the Interop Labs team's further elaboration in the same tweet caused quite a stir. They stated that the Axelar Network, foundation, and AXL token will continue to operate independently, and their development work will be taken over by CommonPrefix.

In other words, the core of this transaction is the "team joining Circle" to drive the application of USDC in the fields of privacy computing and compliant payments, rather than a full acquisition of the Axelar Network or its token ecosystem. The team and the technology are what Circle has acquired. Your original project is of no concern to Circle.

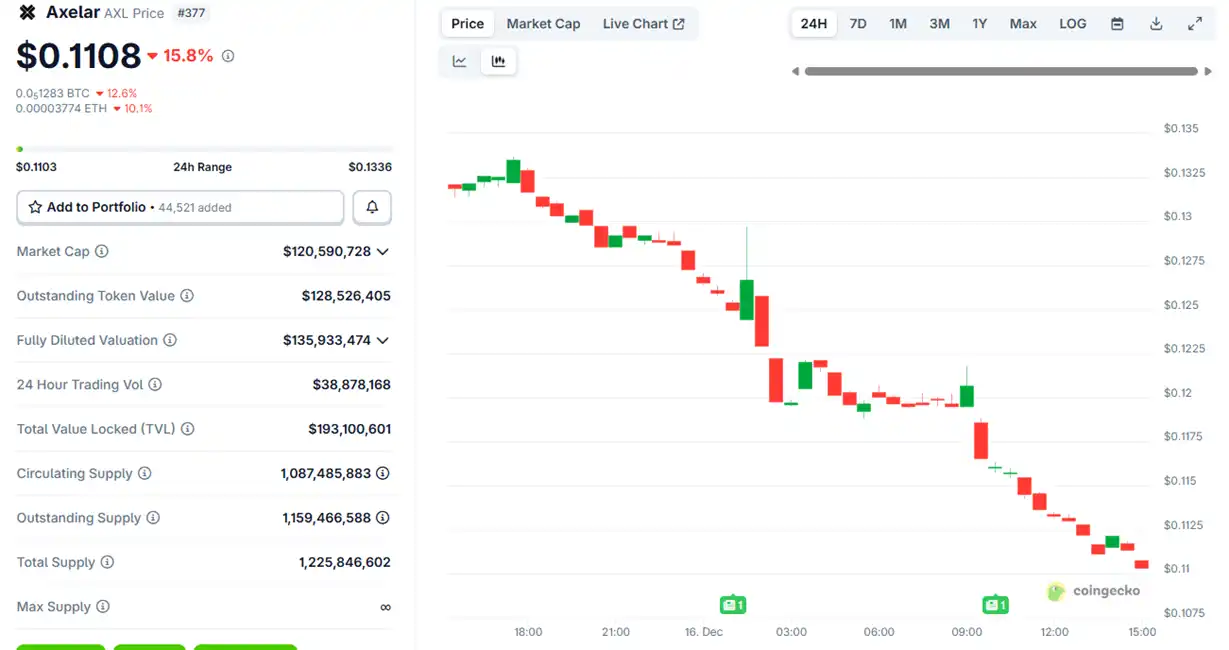

Following the announcement of the acquisition, the price of the Axelar token $AXL initially saw a slight increase before starting to decline, and it has now dropped by approximately 15%.

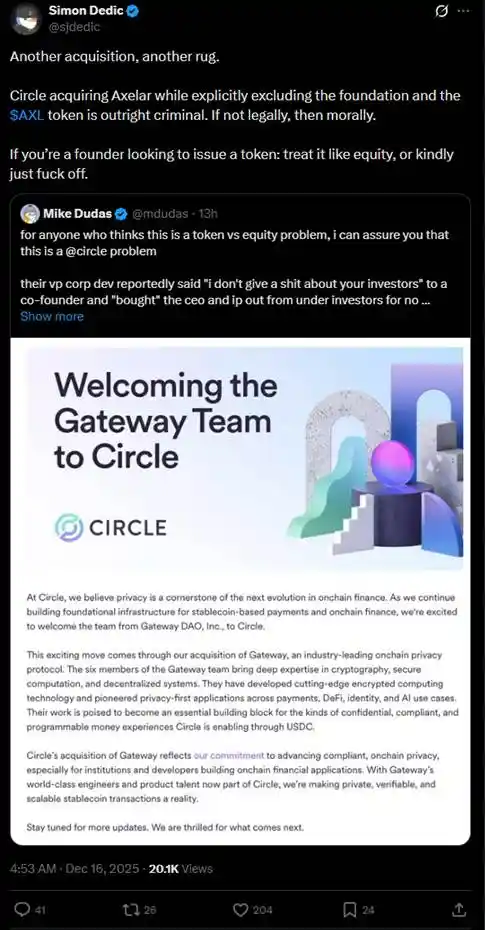

This arrangement quickly sparked a heated debate in the community about "token vs. equity." Many investors questioned whether Circle, by acquiring the team and intellectual property, effectively acquired the core assets while bypassing the rights of AXL token holders.

"If you are a founder and want to issue a token, either treat it like equity or get out."

Over the past year, similar cases of "wanting the team and the technology, but not the token" have occurred repeatedly in the crypto space, causing significant harm to retail investors.

In July, the foundation of Kraken's Layer 2 network, Ink, acquired the decentralized exchange platform Vertex Protocol based on Arbitrum, taking over its engineering team and trading technology stack, including synchronized order book, perpetual contract engine, and money market code. After the acquisition, Vertex closed its services on 9 EVM chains, and the $VRTX token was abandoned. Upon the announcement, $VRTX plummeted by over 75% on the same day, gradually approaching zero (currently valued at only $73,000).

However, holders of $VRTX still have a tiny bit of comfort because during the Ink TGE, they will receive a 1% airdrop (snapshot has ended). Next, there is something even worse: outright nullification with no compensation whatsoever.

In October, pump.fun announced the acquisition of the trading terminal Padre. Upon the announcement of the Padre acquisition, pump.fun also stated that the Padre token would no longer be used on the platform and directly expressed that there were no future plans for the token. Due to the token nullification statement in the final reply of the thread, the token instantly doubled and then sharply fell, with $PADRE currently holding only a $100,000 market cap.

In November, Coinbase announced the acquisition of Solana trading terminal Vector.fun built by Tensor Labs. Coinbase integrated Vector's technology into its DEX infrastructure, but did not involve the Tensor NFT marketplace itself or the ownership of $TNSR, with some of the Tensor Labs team transitioning to Coinbase or other projects.

The trend of $TNSR is relatively stable compared to several examples, characterized by a surge followed by a fall back, with the current price returning to a level expected of an NFT market token and still higher than the low point before the acquisition announcement.

In Web2, it is legal for small companies to be acquired by large enterprises in a "we want the team, we want the technology IP, but we don't want the equity" manner, a situation known as "acquihire." Especially in the tech industry, "acquihire" allows large enterprises to rapidly integrate talented teams and technology through this method, avoiding the lengthy process of recruiting from scratch or internal development, thereby accelerating product development, entering new markets, or enhancing competitiveness. Although disadvantageous to small shareholders, it stimulates overall economic growth and technological innovation.

Nevertheless, "acquihire" must also adhere to the principle of "acting in the best interest of the company." The reason why these examples in the crypto industry have made the community so angry is precisely because the "small shareholders" who are token holders do not agree with the project teams in the crypto industry "acting in the best interest of the company" by being acquired for the better development of the project. Project teams often dream of going public on the stock exchange when the project itself can earn big money, and then when everything is just starting or hitting a dead end, they launch a token to make money (the most typical example being OpenSea). After these project teams make money from the token, they quickly find new homes for themselves, leaving behind the past projects only in their resumes.

So, does the retail investor in the crypto space have to keep gritting their teeth and swallowing the bitter pill? It was also just the day before yesterday that Ernesto, former Chief Technology Officer of Aave Labs, released a governance proposal titled "$AAVE Alignment Phase 1: Ownership," firing a shot in the crypto community to defend token rights.

The proposal advocates for the Aave DAO and Aave token holders to explicitly hold core rights such as protocol IP, brand, equity, and revenue. Aave service provider representative Marc Zeller and others publicly endorsed the proposal, calling it "one of the most influential proposals in Aave's governance history."

In the proposal, Ernesto mentioned, "Due to some events in the past, some previous posts and comments have held strong animosity towards Aave Labs, but this proposal strives to remain neutral. The proposal does not imply that Aave Labs should not be a contributor to the DAO, or lack the legitimacy or capability of contribution, but the decision should be made by the Aave DAO."

According to crypto KOL @cmdefi's analysis, the root of this conflict lies in Aave Labs replacing the front-end integration of ParaSwap with CoW Swap, resulting in fees flowing to Aave Labs' private address thereafter. In response, Aave DAO supporters view this as a form of pillaging, as with the existence of the AAVE governance token, all benefits should primarily flow to AAVE holders or remain in the treasury to be decided by the DAO vote. Additionally, previously, ParaSwap's revenue would continue to flow into the DAO; the new CoW Swap integration changed this status quo, further convincing the DAO that this was a form of pillaging.

This starkly reflects a conflict similar to that of a "shareholders' meeting versus management," once again highlighting the awkward position of token rights in the crypto industry. In the early days of the industry, many projects promoted token "value capture" (such as earning rewards through staking or directly sharing revenue). However, starting from 2020, SEC enforcement actions (such as the lawsuits against Ripple and Telegram) forced the industry to pivot towards "utility tokens" or "governance tokens," emphasizing usage rights rather than economic rights. As a result, token holders often cannot directly share in project dividends—the project's revenue may flow to the team or VC-held equity, while token holders act as powerless stakeholders.

As seen in the examples mentioned in this article, project teams often sell team, technical resources, or equity to VCs or large corporations while also selling tokens to retail investors, ultimately resulting in resource and equity holders taking priority in profits, leaving token holders marginalized or empty-handed. This is because tokens do not have legally recognized investor rights.

In order to circumvent the regulation that "tokens cannot be securities," tokens have been designed to be increasingly "useless." By avoiding regulation, retail investors have once again found themselves in a highly passive and unprotected position. The various incidents that have occurred this year have, in a sense, reminded us that the current issue of the crypto world's "narrative failure" may not actually be that people no longer believe in narratives—narratives are still convincing, profits are still good, but what exactly can we expect when we buy a token?

You may also like

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

Should we escape the peak? The principle of the tail-end market in the stock market

RootData: May 2026 Cryptocurrency Exchange Transparency Research Report

Founder of Baixing.com: My Experience with Claude Code in Fourteen Points

Yang Ge Gary: Agent Economics and AI Microeconomics

When reasoning becomes a scarce resource, who captures its value?

Jensen Huang dramatically "rescues" the South Korean stock market

Stablecoins vs Deposit Tokens: On the surface, they seem like opposing sides, but in reality, they are interconnected

Bitcoin Crash to $50,000 or Bear Trap Before $100,000? Deep Dive for WEEX Traders

How Could the SpaceX IPO Affect Bitcoin, Altcoins season, and Crypto Liquidity?

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.