The Bounce is a Illusion? The Bond Market Has Answered

Original Title: The Bond Market Isn't Buying This Rally. Neither Am I.

Original Author: KURT S. ALTRICHTER, CRPS

Translation: Peggy, BlockBeats

Editor's Note: As the stock market swiftly recovers from the recent sell-off, approaching historical highs, a narrative of "all risks cleared" is once again taking the lead. However, this article reminds us that by only looking at the equity market, it is easy to misjudge the current true environment.

The signals from the bond and oil markets are not consistent: rising interest rates and high oil prices indicate that inflation remains sticky, the Fed's policy space is limited, and geopolitical conflicts have not yet materialized. In contrast, the stock market is pricing in low inflation, rate cuts resuming, manageable costs, and conflict resolution, which are highly idealistic premises.

The author believes that this rebound is more driven by momentum than fundamentals. Fueled by the trading behavior of "fear of missing out on the rally," prices can deviate from reality in the short term, but ultimately, they still need to return to the range determined by macro variables.

When there is a divergence between different asset classes, the real risk often lies not in who is right or wrong, but in how this discrepancy is resolved. The current issue is not whether the market is optimistic, but whether this optimism has already outpaced the data.

The following is the original text:

"Rule 2: Excess in one direction causes an opposite excess in the other direction." — Bob Farrell

The S&P 500 Index has fully recovered all its losses during the US-Iran conflict. As of yesterday, the index was up 1% from February 27 (the day before the first strike on Iran), just a stone's throw away from a new all-time high (less than 1%).

In just 10 trading days, the market has completed a full round trip.

I'll be blunt; if you're only looking at the stock market now, everything seems to be "back to normal." War broke out, the market fell, then quickly rebounded, everything is back on track, and everyone moves forward.

But if you widen your view, this is not the true picture of what's happening.

The bond market has not confirmed this rally.

The oil market has also not confirmed this rally.

When the world's two most important markets are telling a different story from the stock market, this is by no means a signal to be ignored.

So, what is the current stock market pricing in?

For the S&P 500 to be above its pre-war level, the market actually needs to simultaneously believe in the following:

The current oil price is not enough to substantially curb consumption

The Fed will ignore overheating inflation data and still choose to cut rates

Higher raw material and transportation costs will not erode corporate profit margins

The Middle East conflict will be close enough to resolution within six months to no longer pose a risk

Maybe things will really unfold this way. I'm not saying it's impossible. But this is a rather radical set of assumptions, and the data released by the bond and oil markets at present do not support these assumptions.

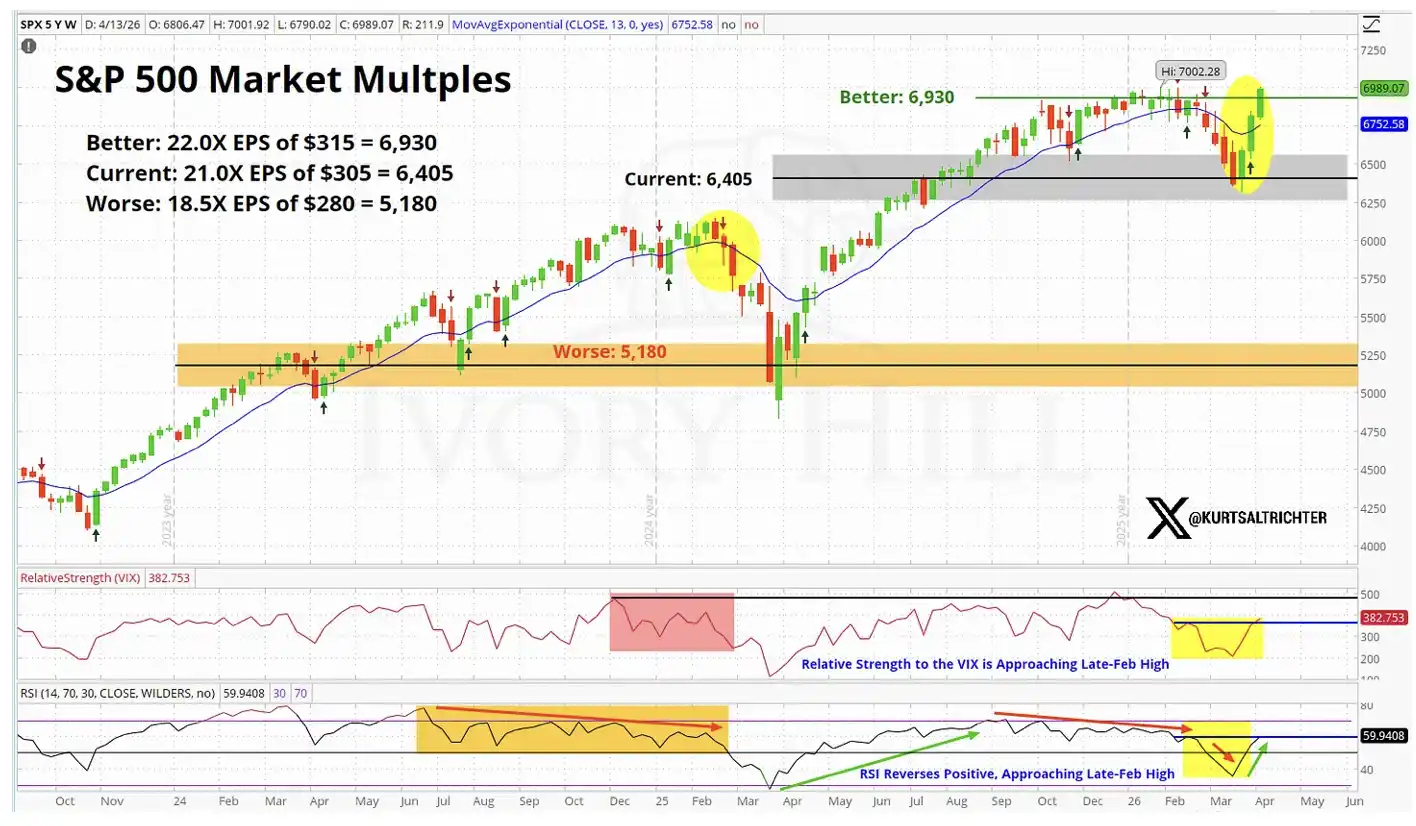

From a fundamental perspective, the stock market's pricing is already close to "perfect expectations."

Let's look at some more specific data

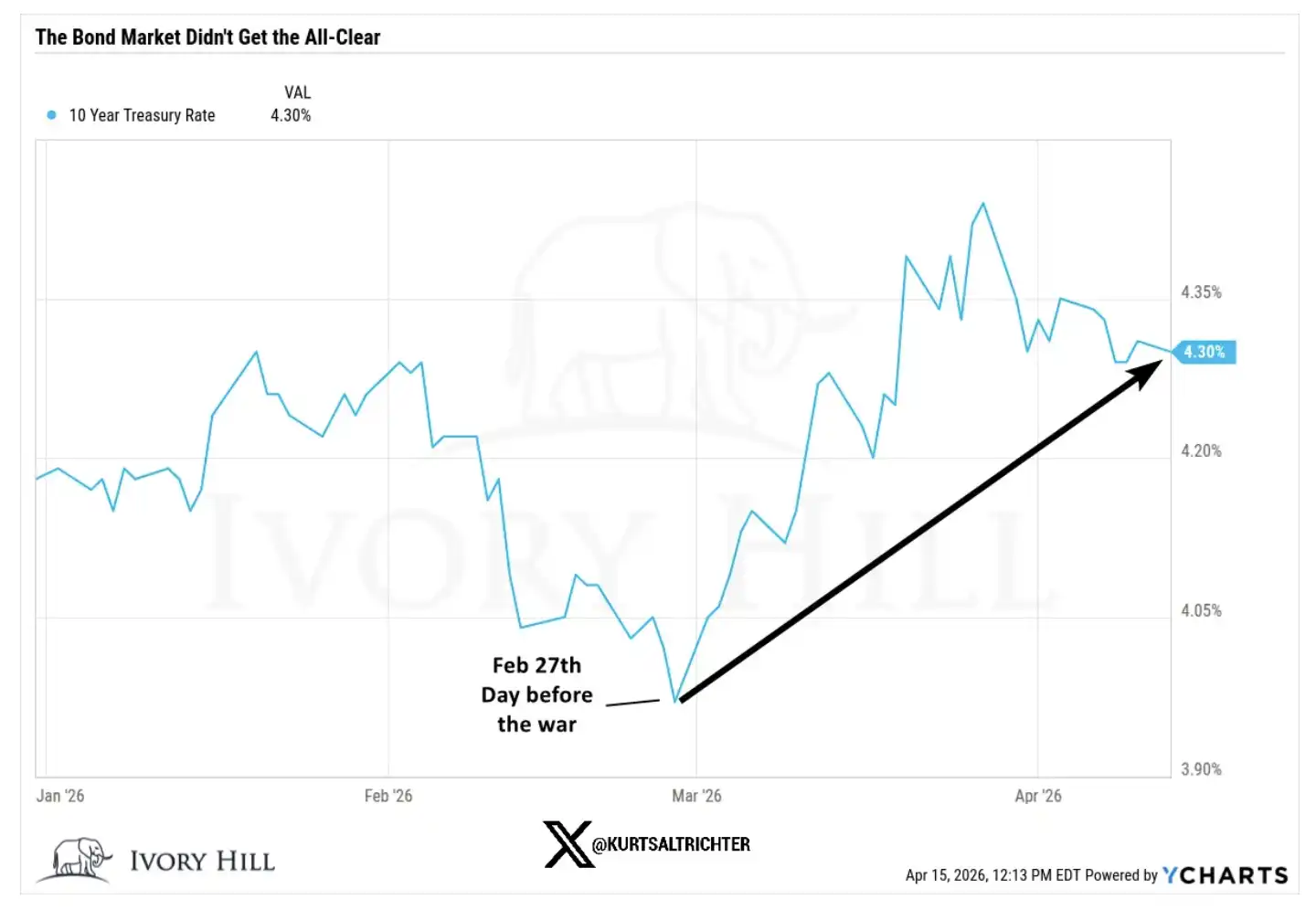

On February 27, the day before the war broke out, the closing figures for key indicators were as follows:

10-Year U.S. Treasury Yield: 3.95%, closing at 4.25% yesterday, up 30 basis points from pre-war levels

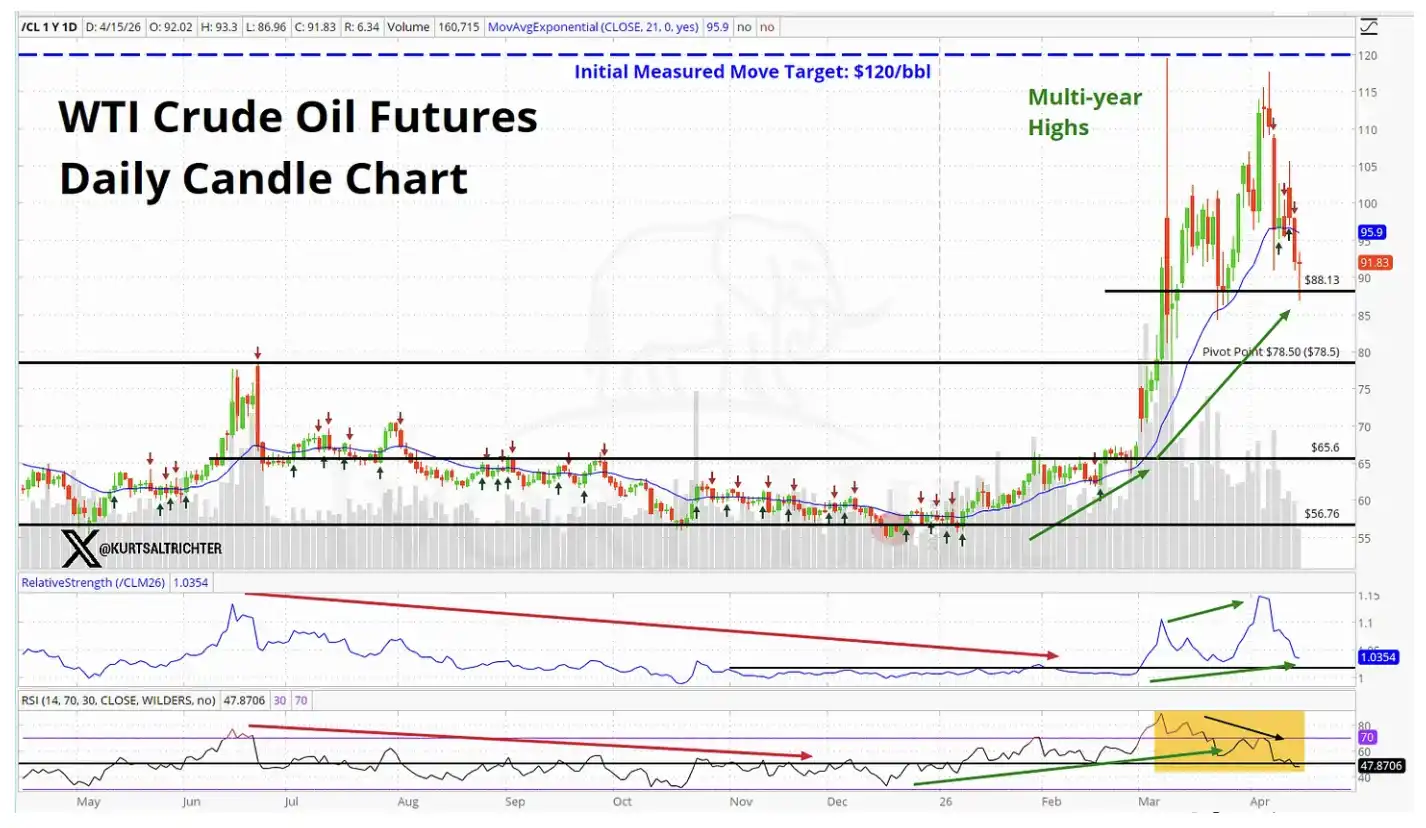

WTI Crude Oil: $67.02, currently about 37% higher than at that time

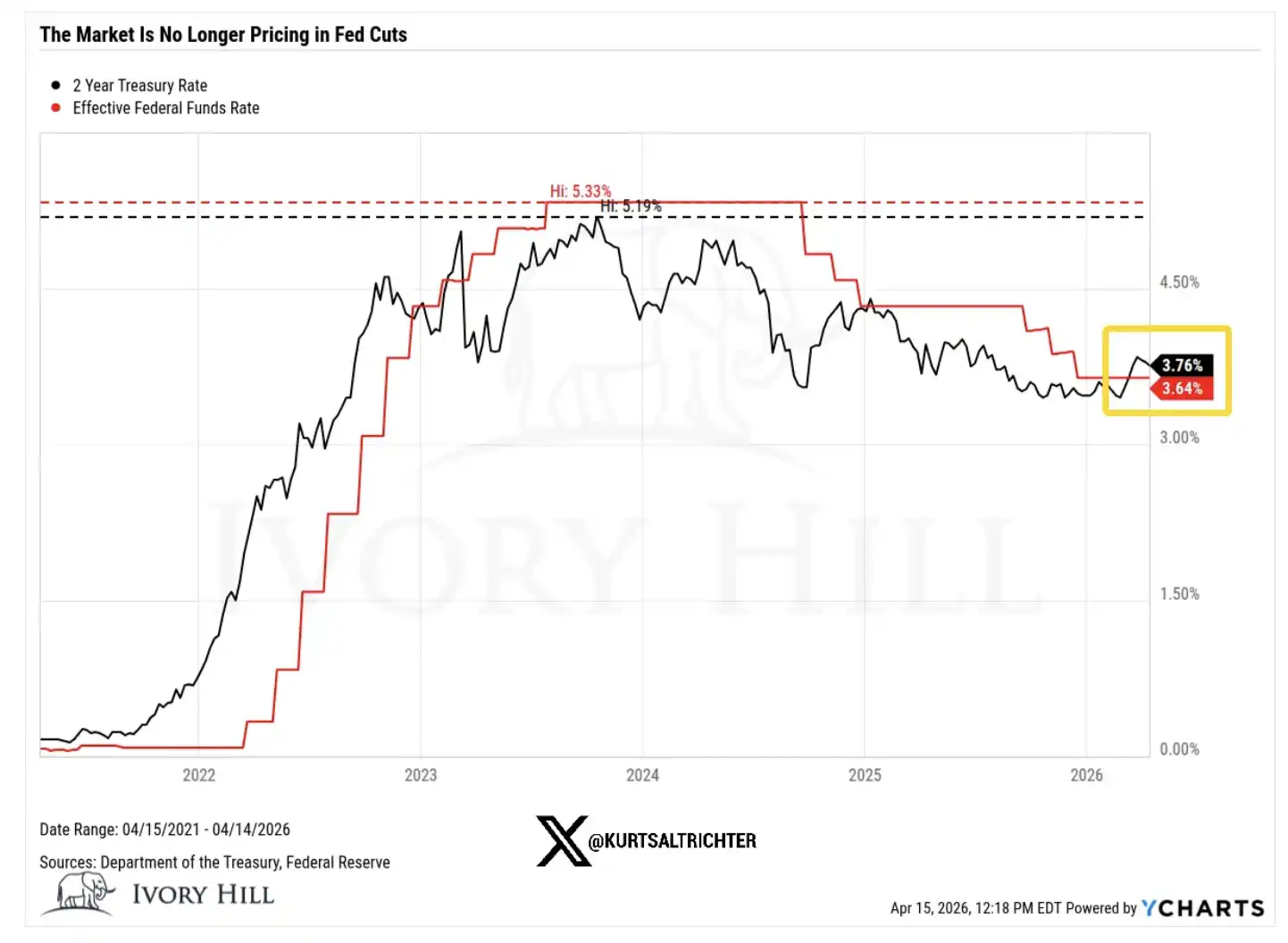

2-Year U.S. Treasury Yield: 3.38%, closing at 3.75% yesterday, up nearly 40 basis points from the pre-war level

Now, let's break down the implications behind these changes one by one.

The 10-year yield rising 30 basis points after the war broke out is not because the bond market is more optimistic about economic growth. Current consumer sentiment is weakening, and confidence remains fragile. This upward rate movement is essentially the bond market quietly pricing in inflation.

The signal it conveys is clear: higher oil prices are transmitting to the overall price system, and the Fed's future policy space may not be as accommodative as the stock market assumes.

Oil prices have risen by 37% in 6 weeks, which is not a reflection of what the market should exhibit when believing that a real, lasting agreement is about to be reached between the U.S. and Iran.

If traders were truly confident in a sustainable ceasefire agreement, oil prices would have already dropped to the $70 range and continued downwards. However, reality tells a different story. Oil prices are still holding at high levels, indicating that the crude oil market has not priced in the same "conflict resolution on the horizon" expectations as the stock market.

Meanwhile, the 2-year U.S. Treasury yield remains 40 basis points higher than pre-war levels, posing a direct challenge to the narrative of "Fed rate cuts incoming."

The 2-year yield is the most sensitive indicator in our interest rate outlook observation, reflecting the Fed's policy path more directly than any other asset. Currently, the signal it is sending is that the Fed's maneuvering room is smaller than the market imagines, which will impact almost all valuation logics supporting this stock market rally.

So, who is making the right call?

The stock market may be right, and I am willing to acknowledge that. If a substantive ceasefire agreement does materialize, bond yields could quickly retreat, and once the supply issue sees a credible resolution, oil prices could also see a significant drop. This wouldn't be the first time the stock market led the way, with other markets playing catch-up or "filling the gap" later on.

But there is another explanation that I believe is currently underestimated.

A significant portion of this rally is not fundamentally driven but rather momentum-driven. Traders are reluctant to short-sell in an uptrend, a behavior that continuously boosts the market. Such buying pressure can indeed prolong the trend more than necessary.

However, it does not alter the underlying logic.

The underlying reality is that oil prices remain high, interest rates are still increasing, and the Fed's room for rate cuts is even more limited than what the bulls require.

Rallies driven by fundamentals are often more sustainable, while those driven by momentum are typically more fragile and short-lived. When considering whether to add positions near historical highs, this difference is especially crucial. As depicted in the market valuation chart above, the current stock market has already priced in a "perfect scenario."

My Actual Assessment

Over the past 10 days, there has indeed been some improvement, and I will not deny that. I am not someone who arbitrarily takes a bearish stance.

However, there is still a significant gap between the pricing of the stock market and the reality reflected in bonds and oil, and this gap has not narrowed. I am closely monitoring this point.

Currently, the stock market is at the most optimistic end of the spectrum; while bonds and crude oil are closer to the middle, reflecting a world where inflation still exists, the Fed has limited policy space, and conflicts are not yet truly resolved.

This divergence will ultimately be resolved, and there are only two paths:

Either a true ceasefire agreement is reached, oil prices fall back to around $70, the Fed gains clear room for rate cuts, ultimately proving the stock market right;

Or none of this materializes, the stock market declines, moving closer to the levels reflected by bonds and oil.

Currently, there is no sign that bonds and oil are converging with the stock market; rather, it seems like the stock market needs to move lower to "align" with them.

The next inflation data will be released on May 12. If my assessment is correct, with CPI above 3.5%, the rate-cut narrative for 2026 will basically come to an end.

If you continue to add leverage at this point, you are essentially betting that everything will develop in the most ideal direction: the war will end smoothly, without any "Trumpian sudden remarks" interference; inflation will remain under control; the Fed will cut rates as planned; and corporate profits will stabilize. All four of these things must happen simultaneously. If any one of them deviates significantly, the market's downward adjustment process is likely to be swift and severe.

On the other hand, I prefer to remain patient rather than chase an uptrend that is being "quietly denied" by the two major asset classes. If the long-term signals point to buying, we will naturally incrementally increase our positions according to the strategy.

And don't forget—the only thing that's certain is that everything will eventually change.

You may also like

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.