MSCI Hardball Strategy: What Did the 12-Page Defense Open Letter Say? As a finance and blockchain translation expert, you are familiar with the slang and terms used in the field. Please translate the following content into English while maintaining th...

Original Title: "Strategy Takes on MSCI: The Ultimate Defense of DAT"

Original Author: KarenZ, Foresight News

The game regarding the development of the Digital Asset Treasury (DAT) industry is still ongoing.

In October, the global index provider MSCI put forward a proposal to exclude companies with 50% or more of their assets in digital assets from its Global Investable Market Index. This move directly threatens the market position of digital asset treasury companies represented by Strategy and could even reshape the entire flow of capital in the digital asset treasury industry.

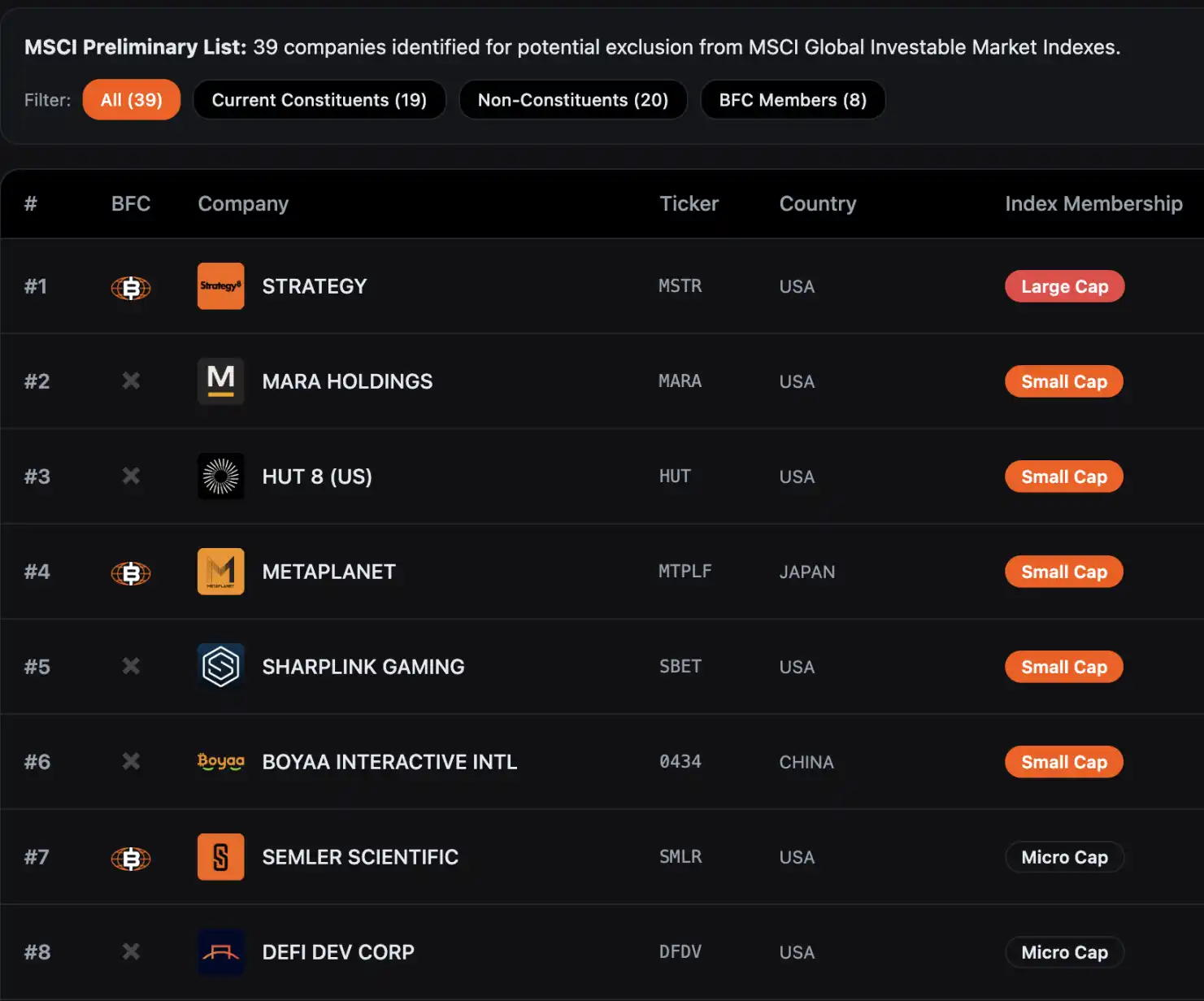

According to data compiled by Bitcoin for Corporations, 39 companies could be excluded from the MSCI Global Investable Market Index. JPMorgan analysts previously warned that the exclusion of just Strategy alone could lead to nearly $2.8 billion in passive outflows, and if other index providers follow suit with this rule, outflows could reach as high as $8.8 billion.

Currently, the consultation period for MSCI's proposal will continue until December 31, 2025, with the final conclusion expected to be announced by January 15, 2026, and any adjustments will be formally implemented in the index review process in February 2026.

Facing this urgent situation, on December 10th, Strategy submitted a strongly worded 12-page open letter to the MSCI Stock Index Committee, jointly signed by the company's Executive Chairman and Founder Michael Saylor and President and CEO Phong Le, clearly expressing firm opposition to the proposal. The letter stated: "This proposal is severely misleading and will have profoundly destructive consequences on the interests of global investors and the development of the digital asset industry. We strongly demand that MSCI fully withdraw this plan."

Strategy's Four Core Defense Arguments

Digital Assets are the Revolutionary Foundation of Financial System Transformation

Strategy believes that MSCI's proposal underestimates the strategic value of Bitcoin and other digital assets. Since Satoshi Nakamoto introduced Bitcoin 16 years ago, this digital asset has gradually grown into a key part of the global economy, with a current market capitalization of around $1.85 trillion.

From Strategy's perspective, digital assets are far more than simple financial instruments; they represent a fundamental technological innovation capable of reshaping the global financial system—enterprises investing in Bitcoin-related infrastructure are building a new financial ecosystem, akin to leading companies in history that deeply engaged with a single emerging technology.

Similar to the 19th-century Standard Oil's deep drilling for oil extraction and 20th-century AT&T's nationwide telephone network construction, these enterprises, through forward-looking investments in core infrastructure, laid a solid foundation for subsequent economic transformation, eventually becoming industry benchmarks. Strategy believes that companies currently focusing on digital assets are following the path of these "technology pioneers" and should not be simplistically dismissed by traditional index rules.

DAT Operates as a Business Enterprise, Not a Passive Fund

This is the core argument Strategy makes—Digital Asset Treasury entities (DATs) are operational businesses with a complete business model, rather than passive investment funds holding Bitcoin. While Strategy currently holds over 600,000 Bitcoin, its core value does not rely on Bitcoin price fluctuations but on designing and launching unique "digital credit" instruments to create sustainable returns for shareholders.

Specifically, the "digital credit" instruments issued by Strategy include various types of preferred stocks covering fixed dividend rates, floating dividend rates, different priority levels, and credit protection clauses. By selling these instruments to raise funds used to accumulate more Bitcoin, as long as Bitcoin's long-term investment return exceeds Strategy's USD-denominated funding costs, it can provide stable returns to shareholders and clients. Strategy emphasizes that this "active operations + asset appreciation" model, distinct from the passive management logic of traditional investment funds or ETFs, should be considered a normal operating business.

At the same time, Strategy also questions why oil giants, real estate investment trusts (REITs), timber companies, and other entities can hold a concentrated single asset class without being classified as investment funds and excluded from the index. Establishing special restrictions only on digital asset companies evidently contradicts industry fairness principles.

A 50% Threshold for Digital Assets Is Arbitrary, Discriminatory, and Impractical

Strategy points out that MSCI's proposal adopts discriminatory standards. Many large companies in traditional industries also hold a single asset class in their assets, including oil and gas companies, real estate investment trusts, timber companies, and power infrastructure enterprises. However, MSCI has only established special exclusion criteria for digital asset companies, which constitutes obvious unfair treatment.

From an implementation feasibility standpoint, this proposal also faces significant issues. Due to the volatile nature of digital asset prices, the same company may repeatedly enter and exit the MSCI Index within a few days due to asset value fluctuations, causing market confusion. Furthermore, differences between accounting standards (U.S. GAAP and international IFRS standards treat digital assets differently) will result in companies with the same business model receiving disparate treatment based on their jurisdiction.

Violating Index Neutrality Principle by Injecting Policy Bias

Strategy believes that MSCI's proposal fundamentally involves a value judgment on a certain type of asset, contravening the basic principle that index providers should maintain neutrality. MSCI claims to provide the market and regulatory bodies with a "comprehensive" coverage of its indices, aiming to reflect the "evolution of the underlying stock market" and should not make judgments on the "merit or suitability of any market, company, strategy, or investment."

By selectively excluding digital asset companies, MSCI is effectively making a policy judgment on behalf of the market, something index providers should avoid.

Contradicting the U.S. Digital Asset Strategy

Strategy particularly emphasizes that this proposal is in conflict with the Trump administration's strategic goal of advancing U.S. leadership in digital assets. The Trump administration signed executive orders in its first week in office to promote the growth of digital financial technology and established a strategic Bitcoin reserve to make the U.S. a global leader in the digital asset space.

However, if MSCI's proposal is implemented, it will directly prevent U.S. pension funds, 401(k) plans, and other long-term funds from investing in digital asset companies, leading to billions of dollars exiting the industry. This not only hinders the development of U.S. digital asset innovative companies but also potentially weakens the U.S.'s competitiveness in this strategic area, running counter to the established government policy direction.

Strategy cites analysts' estimates that Strategy alone could face up to $2.8 billion in passive stock liquidations due to MSCI's proposal. This not only harms Strategy itself but will also have a ripple effect on the entire digital asset ecosystem, such as potentially forcing Bitcoin mining companies to sell assets prematurely to adjust their asset structure, thereby distorting the normal supply-demand relationship in the digital asset market.

Strategy's Ultimate Appeal

Strategy presents two major appeals in an open letter:

First, we hope that MSCI will completely withdraw the exclusion proposal and allow the market to validate the value of Digital Asset Treasury (DAT) companies through free competition, enabling the index to neutrally and faithfully reflect the development trend of next-generation financial technology;

Second, if MSCI persists in "special treatment" of digital asset companies, it should expand the industry consultation scope, extend the consultation period, and provide more comprehensive logical support to explain the reasonableness of the rules.

Strategy is Not a Lone Warrior

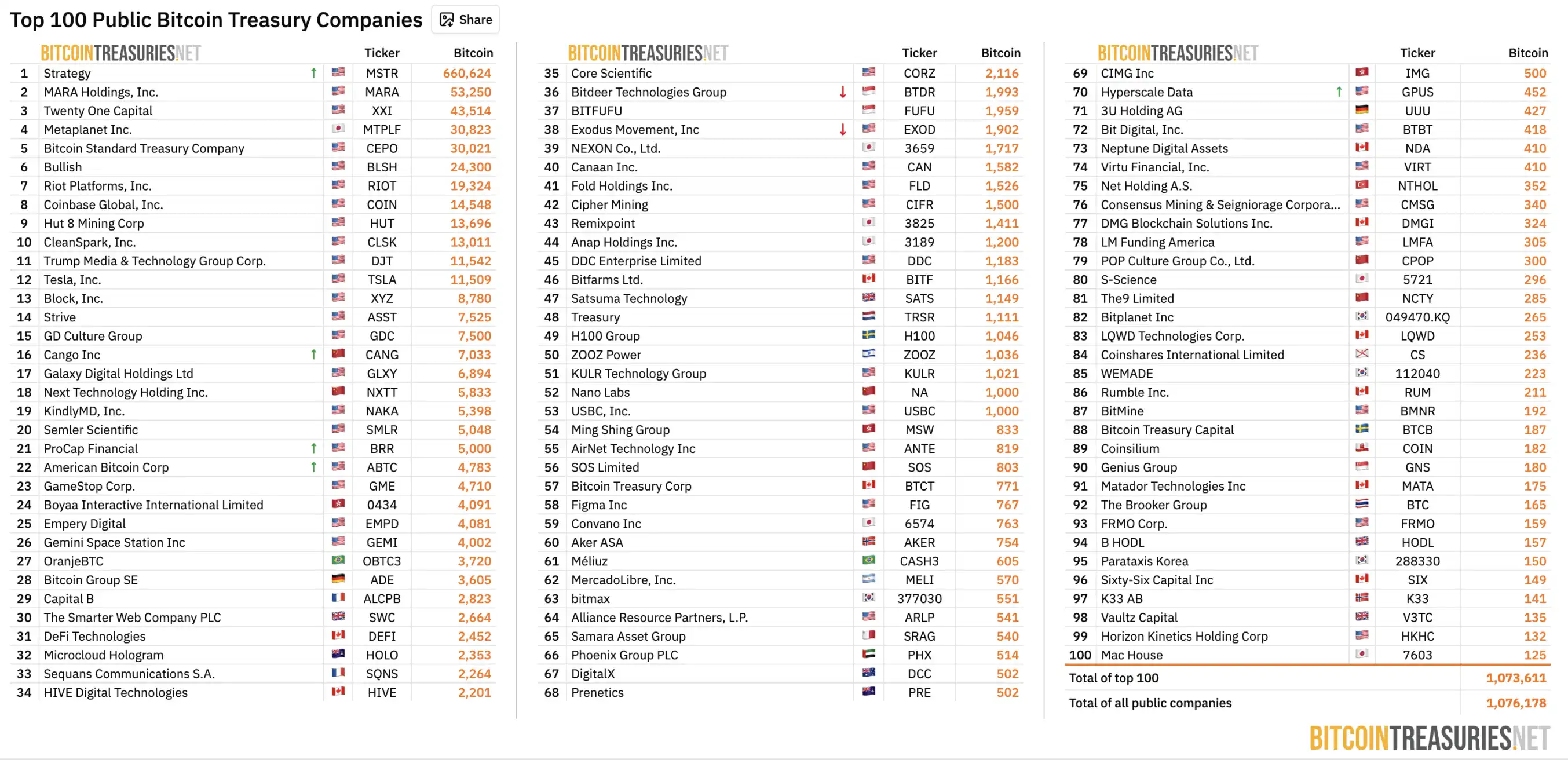

Strategy is not a lone warrior. According to BitcoinTreasuries.NET data, as of December 11, 208 publicly listed companies globally hold over 1.07 million bitcoins, exceeding 5% of the total Bitcoin supply, with a current value of approximately $100 billion.

Source: BitcoinTreasuries.NET

These Digital Asset Treasury companies have become a critical bridge for institutions adopting cryptocurrency, providing compliant indirect exposure to pension funds, endowments, and other traditional financial institutions.

Previously, the Bitcoin-holding public company Strive suggested that MSCI should return the "choice" of digital asset companies to the market. A straightforward solution is to create a "Exclude Digital Asset Treasuries" version of the existing indices, such as the MSCI USA ex Digital Asset Treasuries Index and MSCI ACWI ex Digital Asset Treasuries Index, allowing investors to independently choose their benchmarks through a transparent screening mechanism, thereby preserving the integrity of the index and meeting the needs of different investors.

In addition, the industry organization Bitcoin for Corporations has launched a joint petition calling for MSCI to withdraw the digital asset proposal, advocating that classification should be based on a company's actual business model, financial performance, and operational characteristics, rather than simply drawing a line based on asset allocation. According to the organization's website, 309 companies or investors have currently signed the joint letter, signatories include not only Strategy but also Strive, BitGo, Redwood Digital Group, 21MIL, Btc inc, DeFi Development Corp, and other executives of well-known companies in the industry, as well as many individual developers and investors.

Conclusion

The standoff between Strategy and MSCI is fundamentally a debate on how "emerging financial innovation integrates into the traditional system." As a Digital Asset Treasury (DAT) company, a 'cross-border' entity between traditional finance and the cryptocurrency world, it is neither a pure tech company nor a simple investment fund but rather a new business model built on digital assets.

MSCI's proposal attempts to categorize these complex entities as "investment funds" and exclude them from the index using a "50% asset weight" standard. In contrast, Strategy insists that this oversimplified treatment is a severe misunderstanding of its business nature and a deviation from the principle of index neutrality. As the decision date of January 15, 2026, approaches, the outcome of this game will not only determine the eligibility of several Bitcoin-holding listed companies in the index but will also delineate a crucial "survival boundary" for the future position of the digital asset industry in the global traditional financial system.

References

<1> https://assets.contentstack.io/v3/assets/bltf8d808d9b8cebd37/blt26a263f232aa531c/693976b64c2a191113a60111/strategy-msci-letter.pdf

<2> https://app2.msci.com/webapp/index_ann/DocGet?pub_key=0bZz7Im3vZU%3D&lang=en&format=html

<3> https://x.com/ColeMacro/status/1996930014441623902

You may also like

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

Should we escape the peak? The principle of the tail-end market in the stock market

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.